An International Comparison of National Debt

Using Interest Expenses as a Percent of GDP to Compare National Debts Reveals Important Insights

The views expressed in this blog are entirely my own and do not necessarily represent the views of the Bureau of Labor Statistics or the United States Government.

Today’s blog post is a follow up to last week’s post “A Better Measure of the National Debt.” It is not necessary to read that post to understand this post, but it does provide some context for the measurements used here.

Comparing national debt between countries is a difficult task, as the unique structure of different governments and central banks needs to be accounted for in order to divine meaningful results. The net assets and income of central banks also needs to be taken into account whenever discussing national debts, as central banks’ holdings of government debt can drastically change the financial picture for any country. Central banks also have a critical role to play as payers on another type of often-ignored government debt: bank reserves. The simplest, clearest way to measure and compare national debts is to use net interest expenses, the total amount of interest paid by the government and central bank to private sector, as a share of Gross Domestic Product (GDP).

Looking at debt this way brings to light nuances and truths that are buried by gross national debt figures. It helps illustrate why Japan has no problem paying its debt, at a gross value of more than 200% of GDP, while Italy struggles with a comparatively smaller debt to GDP ratio. It helps illustrate why Germany, which has increased its gross debt to GDP ratio slightly since the 2008 recession, has actually experienced an unprecedented rapid decline in interest costs. Finally, it helps put the “safe asset shortage” and “secular stagnation” in proper context - the cost of debt for high-income countries has never been lower and the historic decline in aggregate demand requires additional fiscal spending to maintain economic growth.

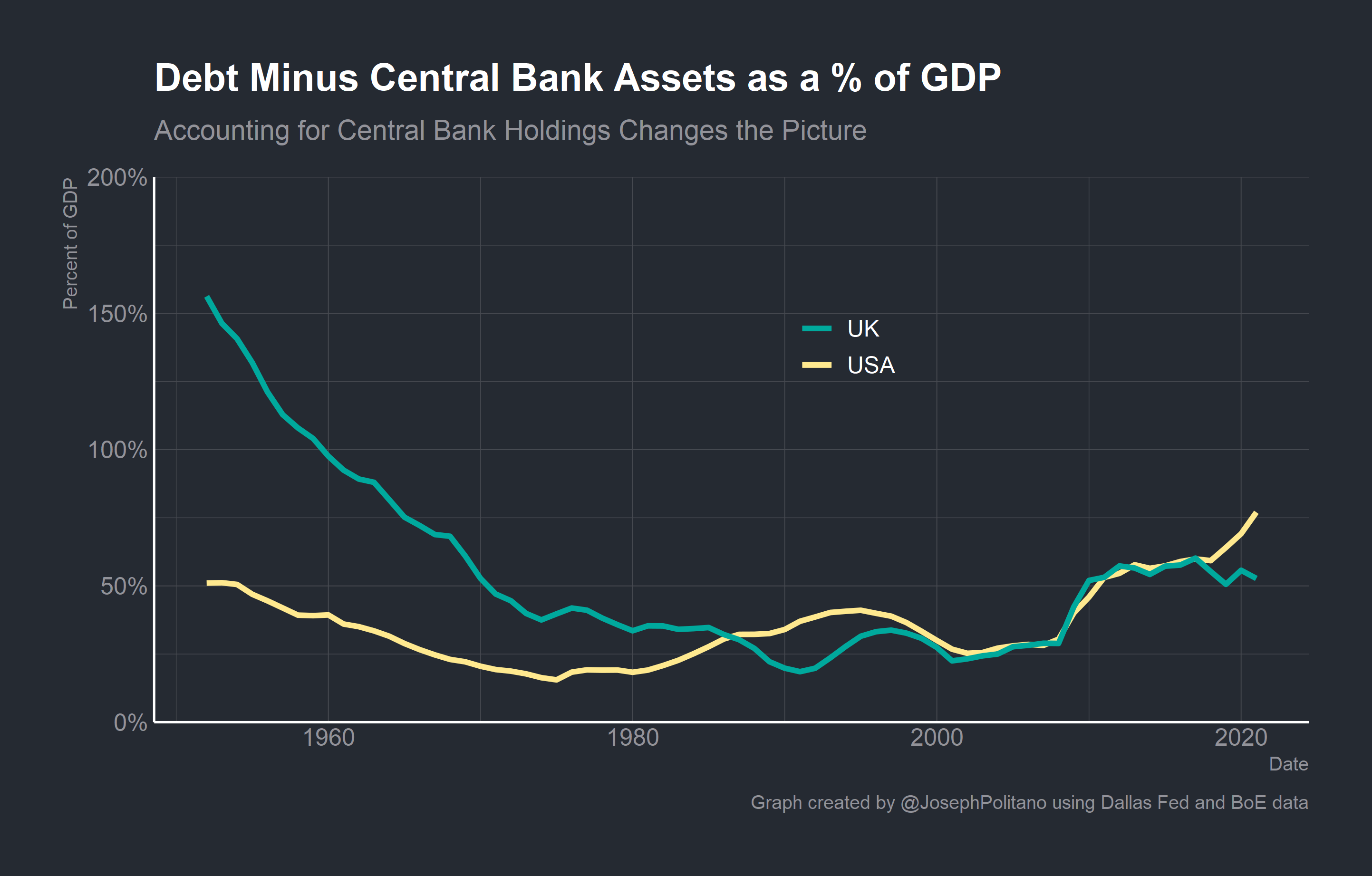

Accounting for Central Bank Assets

The graph above shows national debt minus the central bank balance sheet for both the United States and the United Kingdom. Subtracting the central bank’s balance sheet from the national debt essentially calculates the privately held national debt. Central banks usually have to remit most of their profits from their holdings of government debt and other financial assets back to the national government, although systems differ between countries in important ways that will be discussed later. In essence the government is paying the central bank interest and the central bank must immediately repay that interest back to the government. This is increasingly important as central banks across the world engage in Quantitative Easing (QE), a program where central banks purchase government debt and other assets using a special kind of inter-bank money called reserves. Astute readers of last week’s blog post will remember that the interest paid on reserves makes them essentially another type of government debt, but reserves are unaccounted for here.

Privately held national debt starts out exceptionally high for the UK as a result of World War Two leaving the country with substantial debt and reduced GDP. The UK was essentially able to “grow out” of this debt - while the nominal value of the debt kept expanding and the UK ran consistent deficits, GDP grew much faster than the debt and privately held debt/GDP steadily decreased until it converged with privately held debt/GDP in the US. The two levels remained fairly stable until the financial crisis, at which point they dramatically increased as governments borrowed to stimulate the economy while GDP growth tanked. Only recently have the two countries diverged again as the US borrows extraordinary amounts to fight the COVID-19 pandemic.

Zooming in to the last 30 years and expanding our analysis to include Germany, Italy, and Japan we can see some important additional trends. Japan’s privately held debt/GDP dramatically diverges from the US and UK in the aftermath of the collapse of the Japanese economy in 1991 and the ensuing lost decade. In 2013 the Bank of Japan wholeheartedly committed to their Quantitative and Qualitative Easing program (QQE), whereby the Bank of Japan purchased massive amounts of Japanese government bonds and other financial assets. These purchases were so exceptionally large that the Bank of Japan now holds nearly half of all Japanese debt, leading to the drastic reduction in privately held Japanese debt despite large gross fiscal deficits.

Germany’s privately held debt to GDP ratio, which was always around 50% from the creation of the Euro to the financial crisis, has actually seen an exceptionally large decrease as a result of German fiscal austerity and exceptionally large bond-buying by the European Central Bank (ECB). Due to the structure of the ECB, where profits and assets are distributed based on a “capital key” that measures the population and economic size of Eurozone countries, it is theoretically possible and in fact extremely likely that Germany’s privately held debt/GDP will become negative over the next decade. Essentially, when the ECB buys an Italian bond Germany “owns” about 26% of that bond based on its capital key. If the total assets of the ECB exceeded four times the German national debt, then Germany’s net privately held debt would be negative. To be more precise, Germany’s share of assets on the ECB’s balance sheet would outweigh its national debt, even though some German bonds would still be held by the private sector. Because the ECB’s asset purchase rules require it to purchase relatively proportionate amounts from all Eurozone countries based on their GDP and population, it is possible that the ECB would own nearly all of Germany’s debt. Before the pandemic only a small amount of German debt was privately held by non-central banks. Italy, the supposed fiscal profligate of the EU, has actually shown relatively little increase in privately held debt/GDP since the turn of the millennium. Before the pandemic, Italy had actually run primary surpluses (that is, a fiscal surplus before interest expenses) every year since 1995 except 2009. Additionally, the increase in ECB assets has meant that Italy’s net debt has shrunk slightly even though gross debt has been increasing.

These measures, as I explained in the previous blog post, present an incomplete picture of the size of any country’s financial obligations. For one, these measures of gross debt do not in any way account for the interest rates that countries pay on their debts, a critical element in measuring the cost of debt. They also do not take reserves, essentially another government debt instrument, into account at all. Finally, they require making fundamentally arbitrary distinctions about whether pension obligations and entitlement programs are debt or whether loans from the government or dedicated revenue streams are assets. Instead, the best measure for international and intertemporal analyses of national debt is interest expenses net of remittances from the central bank.

Comparing Net Interest Expenses

The primary advantage in this case is their simplicity - no arbitrary accounting distinctions must be made in order to compare interest expenses between countries as long as you net out remittances from the central bank. As I explained last week, accounting for these remittances essentially calculates the governments total interest expenses to the private sector:

These remittances are the difference between the income the Federal Reserve receives on its portfolio of mostly Treasury securities and the interest it pays on reserves. Since the Federal Reserve is required to remit any profits it receives, the money the Department of the Treasury pays on securities held by the Fed is not true interest expense. Only the interest paid on reserves, which are held by private banks, is actually a form of government interest expense. The Federal Reserve almost always takes in more money from the Treasury than it gives out to private banks because Treasury bonds are riskier long term assets that pay higher interest rates than low risk short term reserves. Since these profits remitted to the Treasury represent the gap between interest paid to the public on reserves and interest paid to the Federal Reserve on treasuries, subtracting remittances from federal interest expenses generates the government’s total net interest expenses to the public.

It is worth noting that not all central banks follow the clean setup of America’s Federal Reserve where all profits are remitted directly back to the Treasury. In the EU, the ECB distributes profits to National Central Banks (NCBs) like Germany’s Deutsche Bundesbank and Italy’s Banca d’Italia. These NCBs follow unique rules - Deutsche Bundesbank distributes all of its profits back to the German government while Banca d’Italia pays corporate tax and distributes most profits to the Italian government. Bank of Japan follows a similar structure as Banca d’Italia. Regardless of the method, the result is the same - interest expenses net central bank remittances represent the best measure of the national debt.

The graph above shows the net interest expenses for both the US and the UK. The burden of the post-WWII debt on the UK is much clearer here; it took until 1990 for the cost to service the UK’s debt to match that of the US. The recent divergence is also notable, as even though the UK and US’s privately held debt to GDP moved in lockstep from 2000 to 2018, the cost to service the UK’s debt was substantially higher. This is partly evidence of what is usually referred to as America’s “exorbitant privilege.” Since the dollar is the world’s reserve currency and is used for international transactions across the world, the US can reap financial benefits from the increased global demand for the dollar and dollar-denominated safe assets like US government debt.

Including Italy, Germany, and Japan provides some additional interesting insights. For one, Germany’s interest expenses have declined to only 0.5% of GDP in recent years. Given the negative nominal interest rates throughout much of the Eurozone and the incredibly small debt burden Germany has, the German government’s unwillingness to use strong fiscal policy to combat the Great Recession and the Euro crisis becomes even less excusable. The EU has had a generalized shortfall of aggregate demand for nearly 15 years that has caused dramatic drops in GDP per capita growth, and part of the reason is the unwillingness by national governments to use necessary fiscal stimulus. Japan is another interesting case; despite nominally being one of the most indebted countries in the world, its net interest expenses are substantially smaller than Italy’s and marginally smaller than the UK’s. Italy is the extreme outlier here: despite rapidly shrinking interest expenses, the cost to service the Italian debt is twice that of the next most expensive country. Why is this?

The important X-factor is interest rates and central bank policy. It is worth noting that Italy had much more substantial debt than Japan during the 1990s, when EU interest rates were significantly higher than in Japan due to the latter country’s “lost decade”. However, today both Italy and Japan have similar debt burdens, negative interest rates, and QE policies, so why haven’t net interest expenses converged? The structure of the ECB has actually precluded the kind of extremely large asset purchases and extremely low long-term interest rates that keep the debt in check in Japan. The EU cannot buy Italian bonds only, meaning that in order to boost demand and output in Italy the EU must buy a combination of Italian, French, German, etc. bonds. Since these countries all have different amounts of debt, the ECB is prevented from targeting a single long-term interest rate across the Eurozone without purchasing bonds disproportionately from highly-indebted countries like Italy and Spain. The result is that there is a substantial “spread”, or difference in yield, in equivalent bonds from different EU countries. As of right now, the yield on Italian 10 year bonds is about 0.63%, while the yield on German 10 year bonds is -0.46%! By contrast, Bank of Japan has been successfully targeting 0% yield on all Japanese bonds with a maturity under 10 years.

To be clear, these interest rate targets and asset purchases are not “artificial meddling” or by the central bank. In fact, central banks must undertake policy actions, even so-called “unconventional policy” like QE or Yield Curve Control (the practice of targeting a certain interest rate for long-term bonds), that allow them to achieve their policy goals. The fact is NGDP growth, inflation, and income growth in the EU and Japan have been below their central banks’ targets for a long time now, meaning policy has been too tight, not too loose. The difference is that while Japan has been able to target long term interest rates to boost lending and enable fiscal borrowing to combat deflation, Italy is unable to do so under the current ECB policy regime. In fact, both countries need more expansionary monetary and fiscal policy to keep NGDP growth and labor income growth at their highest possible levels.

Just how important has central bank policy been for interest expenses? The graph above shows net interest expenses for the US, Italy, and Japan in solid lines and interest expenses not including central bank remittances in dashed lines. While the gap is fairly significant and growing for all three countries, remittances almost never exceed 0.5% of GDP. Instead, the central bank’s interest rate policy likely makes the biggest difference on the cost of debt, as seen by the large gap between Italy and Japan’s interest expenses.

The Safe Asset Shortage and Secular Stagnation

Since 2008, two concept have emerged to explain both the extra-low interest rate environment and the long-term decline of economic growth in advanced economies.

The first is the idea of a “safe asset shortage.” My friend Taylor has the definitive blogpost on the concept if you want to read about it, but to make a long story short the rapid economic growth of low-income nations and the rise of a global middle class has dramatically increased demand for so-called safe assets like US dollars. The result has been near insatiable demand for dollars, euros, pounds, yen, and financial assets denominated in these currencies that has helped keep inflation and interest rates low in high-income countries despite their growing nominal debts and money supplies. Although I dislike reasoning from unobservable variables, this can be thought of as a long-term reduction in the “natural” rate of interest for these countries. This means that central banks can lower nominal rates to near or below zero with little to no adverse increases in inflation. The safe asset shortage may be partly responsible for pinning many central banks to the effective lower bound, the negative nominal interest rate central banks cannot go below without forcing private banks to pass on negative rates to their depositors.

The second idea is “secular stagnation.” The concept, which dates back to the 1930s but was brought back into the popular discussion by economist Larry Summers, is that market based economies can get stuck in a long-term cycle of extremely low or zero GDP growth. Persistent shortfalls in private sector demand caused by endemic decreases in population growth, investment, household incomes, or other variables leave economic growth constantly below potential and push the “natural” interest rate downward until it hits the effective lower bound. With less economic growth, investment shrinks, further reinforcing the cycle of decreasing economic growth. This is the situation Japan and Italy have found themselves in: little to no nominal growth with below-target inflation and persistent shortfalls in aggregate demand.

Both of these scenarios reduce the cost of fiscal borrowing and increase its urgency. The decline in “natural” long term rates decreases the costs of deficit financed government investment, while the below-potential economy means that the fiscal multiplier is positive and any increase in government spending will increase GDP by more than the new debt.

I am not a die-hard believer in either secular stagnation or the safe asset shortage. I believe each story has some merit, but that the primary reason many high-income economies remain below potential is overly tight monetary policy. Bank of Japan’s abrupt and aggressive rate hikes were the onset for the bursting of the Japanese asset bubble and the three “lost decades”. The ECB’s 2011 rate hikes and its unwillingness to back member countries’ sovereign debt exacerbated the Great Recession and helped cause the Euro crisis.

We can see that debt, properly measured, in Japan and Italy has been steadily decreasing while demand remains weak and central banks remain unwilling to venture further into negative interest rates. The answer is simple: Japan and Italy must pursue aggressively expansionary fiscal policy. By exploiting the large fiscal multiplier and the low cost of debt, fiscal policy can spur private investment and economic activity, put people back to work, and bring these economies back onto the nominal GDP growth path that bad monetary policy took them off of.

——————————————————————————————————————

A special thanks to Dr. Jöerg Bibow, who wrote the working paper “Unconventional Monetary Policies and Central Bank Profits: Seigniorage as Fiscal Revenue in the Aftermath of the Global Financial Crisis” that was a major source for this post and who was kind enough to answer my questions via email.

Blaming the Japanese financial crisis on the BOJ interest rate policy is rather lazy analysis. It ignores the deregulation underway in the 1980s (pushed on it by the US) and the build up of private debt. BOJ window guidance was either relaxed or became ineffective in the deregulated environment—depending on who you ask. Credit was driving up asset prices—especially real estate—because banks were making loans hand over fist. Banks went bad because they were increasingly making bad loans both domestically and abroad, not merely because the BOJ tightened credit conditions. That was apparent to the market before the rate hikes. If you look at the change in total credit to the private sector from BIS for that period, it was declining well before BOJ increased rates. So the asset bubble was already bursting as credit pulled back. It’s correct to argue the BOJ misstepped by increasing the rate when it should have done the opposite, which it had to do anyway, but it wasn’t the approximate cause of the crisis itself. It was a Minskyan crisis just like the GFC.

“Lost decades” were due to missteps in fiscal policy by raising taxes—much like the US in 2011 after the GFC but by cutting fiscal support.