Banks Face a New Challenge

Rising Rates and Quantitative Tightening Put American Banks in New Territory

Thanks for reading! If you haven’t subscribed, please click the button below:

By subscribing you’ll join over 18,000 people who read Apricitas weekly!

Otherwise, liking or sharing is the best way to support my work. Thank you!

The modern US financial and monetary regime was built in the wake of the 2008 financial crisis—and therefore it was designed to restore financial stability and promote credit creation amidst a flagging economy. Throughout most of the 2010s, the dominant state for the US banking system was low-interest rates, large amounts of Quantitative Easing, weak credit creation, and low inflation. Now, however, commercial banks face a different challenge.

Today’s environment of high inflation, rising interest rates, and Quantitative Tightening presents somewhat uncharted territory for a commercial banking system that has been redeveloped over the past decade. Short-term interest rates are at the highest levels in nearly 15 years, 30-year fixed mortgage rates have surged, deposits are shrinking rapidly, and financial conditions are broadly worsening.

The good news is that much of the macroprudential framework built up over the last decade still applies today—Federal Reserve stress tests suggest that banks could still survive a catastrophic global recession in today’s environment—but analyzing how banks are being pushed and responding to shifting circumstances is critical to understanding credit conditions and the broader US economic outlook. Banks mediate large parts of the Federal Reserve’s inflation-fighting tools, so their risks and behavior carry important implications for the broader economy. And as we enter into a new macro-financial situation it’s important to keep abreast of shifts within the banking system.

QT, Quantitatively Speaking

For just the second time in 20 years, the Federal Reserve is making a concerted effort to shrink its balance sheet size through Quantitative Tightening. The balance sheet growth that occurred during the COVID-19 pandemic is being unwound as the Fed switches from prioritizing financial stability and credit creation to deliberately hurting financial conditions as part of its battle against inflation.

QE, as an asset swap, is arguably most relevant in its role of credibly guiding the future path of interest rates and rebalancing private sector balance sheets towards riskier assets. In other words, the size of the Fed’s balance sheet is less important than how it’s used and what it signals. QT just has the same but opposite effects—removing the guidance that capped interest rate expectations and forcing the private sector to rebalance towards safer assets. Since the start of QT we have seen financial conditions worsening, increasing interest rate volatility, and rising long-term interest rates—so the program is likely having some of its intended effects (although it’s hard to disaggregate the effects of short-term rate hikes and signaling against the actions of QT).

However, quantitative tightening does also have direct effects on the plumbing that underlies the commercial banking system—in particular by driving down the quantity of bank reserves. Reserve balances (including the US Government’s Treasury General Account (TGA)) have dropped nearly $1.5 Trillion since their peak in March 2021 and are still falling.

The real story is the meteoric rise of the Fed’s Overnight Reverse Repo Facility (ON-RRP) which is providing a floor underneath interest rates by essentially granting nonbank financial institutions a risk-free return on their dollar assets that is slightly below the interest paid on bank reserves. Right now the Fed has $2.5T in obligations through the ON-RRP facility, highlighting its growing importance in governing short-term interest rates and Treasury yields. This hiking cycle also marks the deployment of a complimentary Standing Repo Facility (SRF) designed to backstop money markets in the other direction and prevent the kind of cash shortages that caused havoc in 2019.

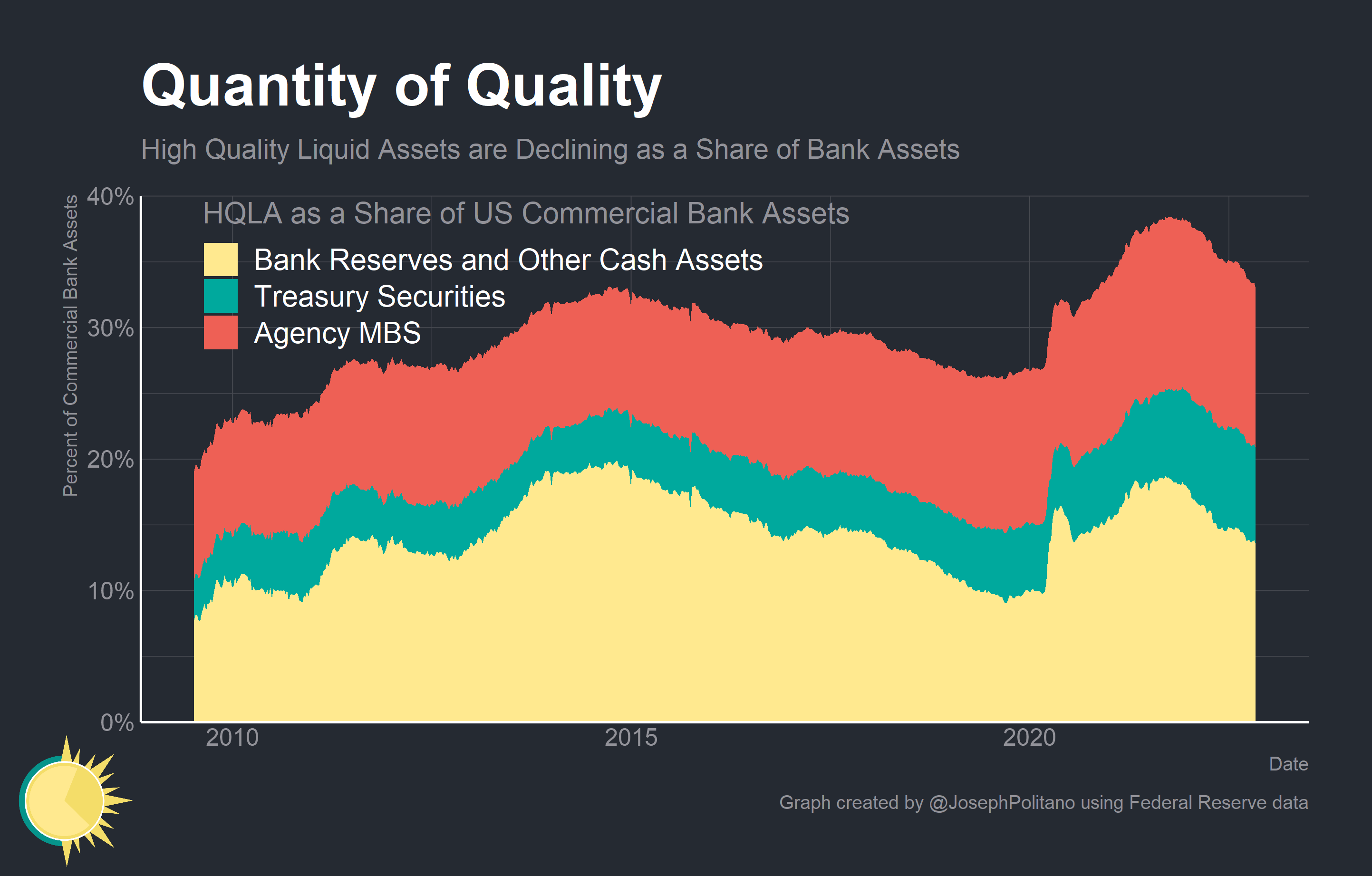

This year has also seen a large decrease in the share of banks’ assets devoted to high-quality liquid assets (HQLA), although they still remain above pre-pandemic levels. The massive rise in bank reserves alongside the more binding nature of liquidity and leverage requirements pushed banks into safer assets, but that is starting to unwind as deposit and reserve levels shrink.

Still, commercial bank assets are stalling—not falling—right now amidst a historic rise in the nominal value of bank loans and leases. Besides the Paycheck Protection Program (PPP) driven lending at the start of the pandemic, the second quarter saw the fastest nominal growth in “loans and leases” since the Great Recession. So what’s behind the massive rise in lending?

{kind=link}

{kind=link}