Can a Strong Dollar Fix Inflation?

Probably Not, At Least on its Own

Thanks for reading! If you haven’t subscribed, please click the button below:

By subscribing you’ll join over 17,000 people who read Apricitas weekly!

Otherwise, liking or sharing is the best way to support my work. Thank you!

Since early 2021, the dollar has been practically unstoppable. Due to a combination of global energy crises, terms-of-trade shocks, tightening US monetary policy, relative US economic strength, and a global flight to safety the dollar has appreciated significantly compared to most other major currencies. But is the dollar strong enough to stop inflation back at home?

The answer is, unfortunately, almost certainly not—at least on its own. Pinning down an exact measure of the exchange-rate pass-through ratio (the amount by which a movement in exchange rates affects consumer prices) is extremely difficult given the changing nature of the economy and the confluence of factors driving today’s exchange rate shocks. However, virtually no realistic estimate will generate the kind of import price reduction necessary to bring inflation down to normal—mostly due to the simple fact that imports constitute a limited subset of US household consumption and GDP.

But thinking about exchange-rate pass-through is critical for understanding the global nature of inflation dynamics. Most places outside America have more to worry about regarding exchange rate pass-through and will therefore have to be more attuned to US monetary policy decisions.

Picking Apart Pass Through

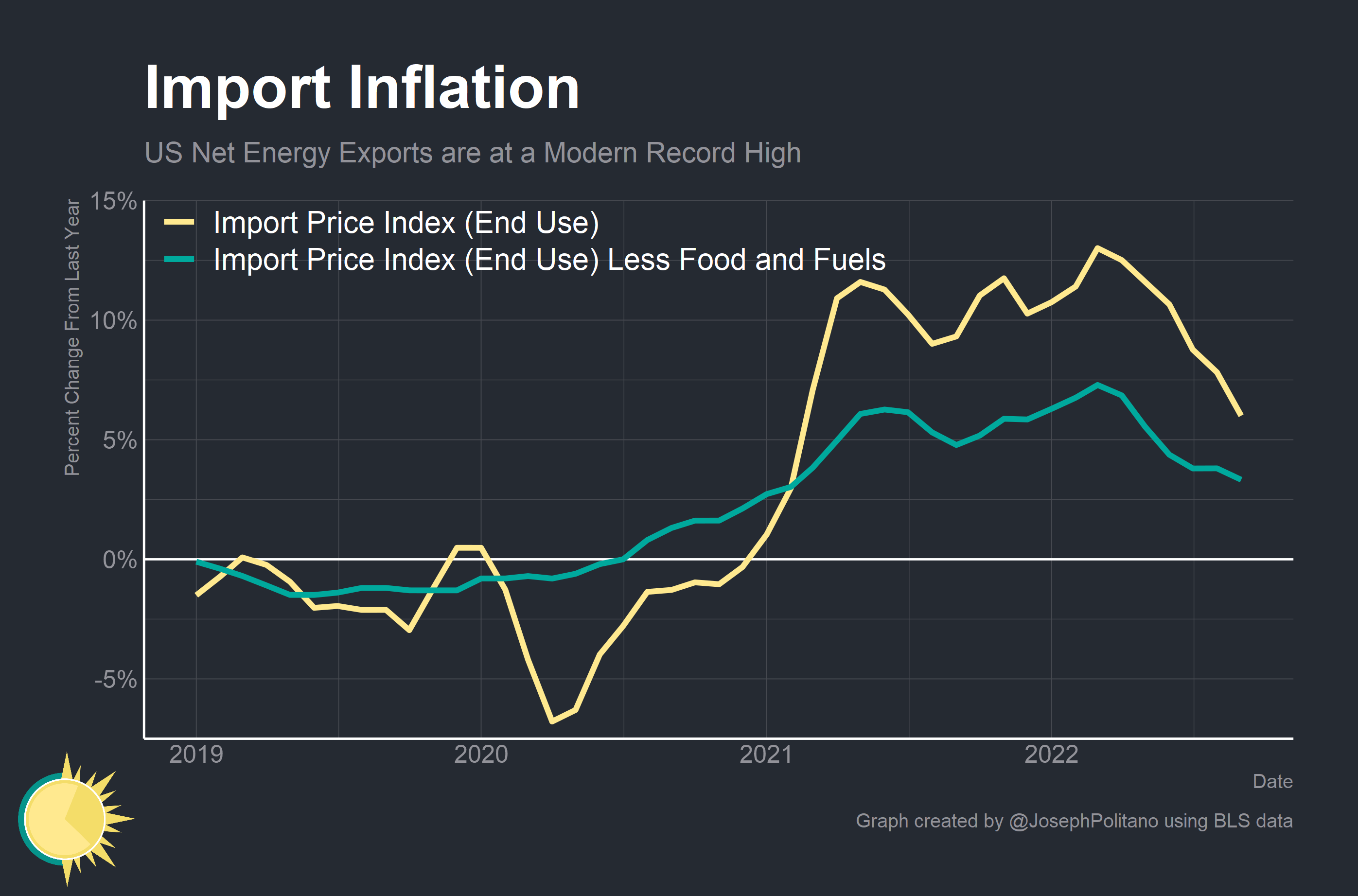

The general idea behind exchange-rate pass-through is that a rise in the value of the dollar should lower the prices of America’s imported goods and thereby counteract inflation. It is, for example, a great time for Americans looking to buy Japanese candies or French wines—currency appreciation means that a dollar goes farther in buying items with sticker prices in Yen or Euros.

However, low exchange-rate pass-throughs for high-income nations (especially the United States) have arguably been a defining feature of modern foreign exchange regimes. Jašová, Moessner, and Takáts (2016) from the Bank for International Settlements estimated that the exchange rate pass-through for high-income nations was functionally zero before the financial crisis and rose to only about 0.05 by late 2018. That is, a 10% depreciation in the trade-weighted exchange rate would lead to about a 0.5% increase in the consumer price index.

The fundamental reason for this is that in most high-income nations the cumulative share of imports in final consumption is relatively low. Total imports of goods and services are only about 15% of US GDP, but even this overstates imports’ true share of consumption. Some imports are for capital goods whose prices don’t feed immediately into consumption, and some imports are for intermediate inputs that go into products that America then re-exports. Accounting for this, a 2019 research note from the San Francisco Fed estimated that imports only composed about 10-11% of US consumption (Hale, Hobijn, Nechoi, Wilson 2019).

A research note from the Kansas City Fed’s Johannes Matschke and Sai A. Sattiraju applied the import share of consumption estimate from the SF Fed’s note to a simple model of the relationship between import prices and exchange rate fluctuations—their estimates were that dollar appreciation had shaved less than 0.2% off of core PCE inflation by August. A further 5% appreciation in the dollar, about in line with what we’ve seen since August, would reduce inflation by 0.3-0.4% in 2023 in their model. That’s fairly sizable, but not enough to bring core PCE inflation from its current 5% levels back to the Fed’s 2% target—at least not on its own.

Keep reading with a 7-day free trial

Subscribe to Apricitas Economics to keep reading this post and get 7 days of free access to the full post archives.