CPI Inflation Was 6.2% Over the Last Year. What Does Future Inflation Have In Store?

Future Inflation Dynamics Will Look Very Different From Current Inflation Dynamics

The views expressed in this blog are entirely my own and do not necessarily represent the views of the Bureau of Labor Statistics or the United States Government.

This is the second post in a new series where I will be breaking down regular economic data releases like inflation, employment, labor turnover, GDP, industrial capacity, and so on in addition to my usual Saturday posts. Expect 2-3 short breakdowns on an irregular schedule each month. Any input or feedback on these breakdowns is welcome as they are a work in progress.

The Consumer Price Index (CPI) rose by 0.9% in October, making the year-on-year CPI inflation 6.2%. Core inflation, meaning CPI excluding food and energy, rose by 0.6% month-on-month and 4.6% year-on-year. Prices for used cars and trucks, which have grown almost 40% since 2020, jumped up 2.5% in October. Fuel oil prices rose a staggering 12.3% in the month, with gasoline alone rising 6.1%. Food prices rose 0.9% and shelter prices, which make up almost a third of CPI, rose 0.5% as well. CPI has significantly exceeded its prior 2% trend, although it is critical to note that the Federal Reserve targets 2% inflation on the Personal Consumption Expenditures Price Index (PCEPI), which tends to increase less than CPI.

Current inflation dynamics are primarily driven by massive, nearly unprecedented price growth in the goods sector. As the pandemic abates, supply chains renormalize, and consumers shift their spending to services, this inflation dynamic will prove to be transitory. This will mean price decreases in the goods sector that are offset by price increases throughout the service sector, making for generally lower inflation—so long as nominal income growth remains on-trend.

The Current Inflation Situation

The pandemic has driven an unprecedented surge in spending on goods as cooped-up consumers throughout America try to make the best of lockdown and work from home. Spending that would have gone to leisure and hospitality, restaurants, or travel has instead gone into additional consumer and durable goods. As much as supply chains appear strained, it is worth acknowledging that they are operating under unprecedented order volumes. In other words, this is a crisis of abundance rather than a crisis of scarcity.

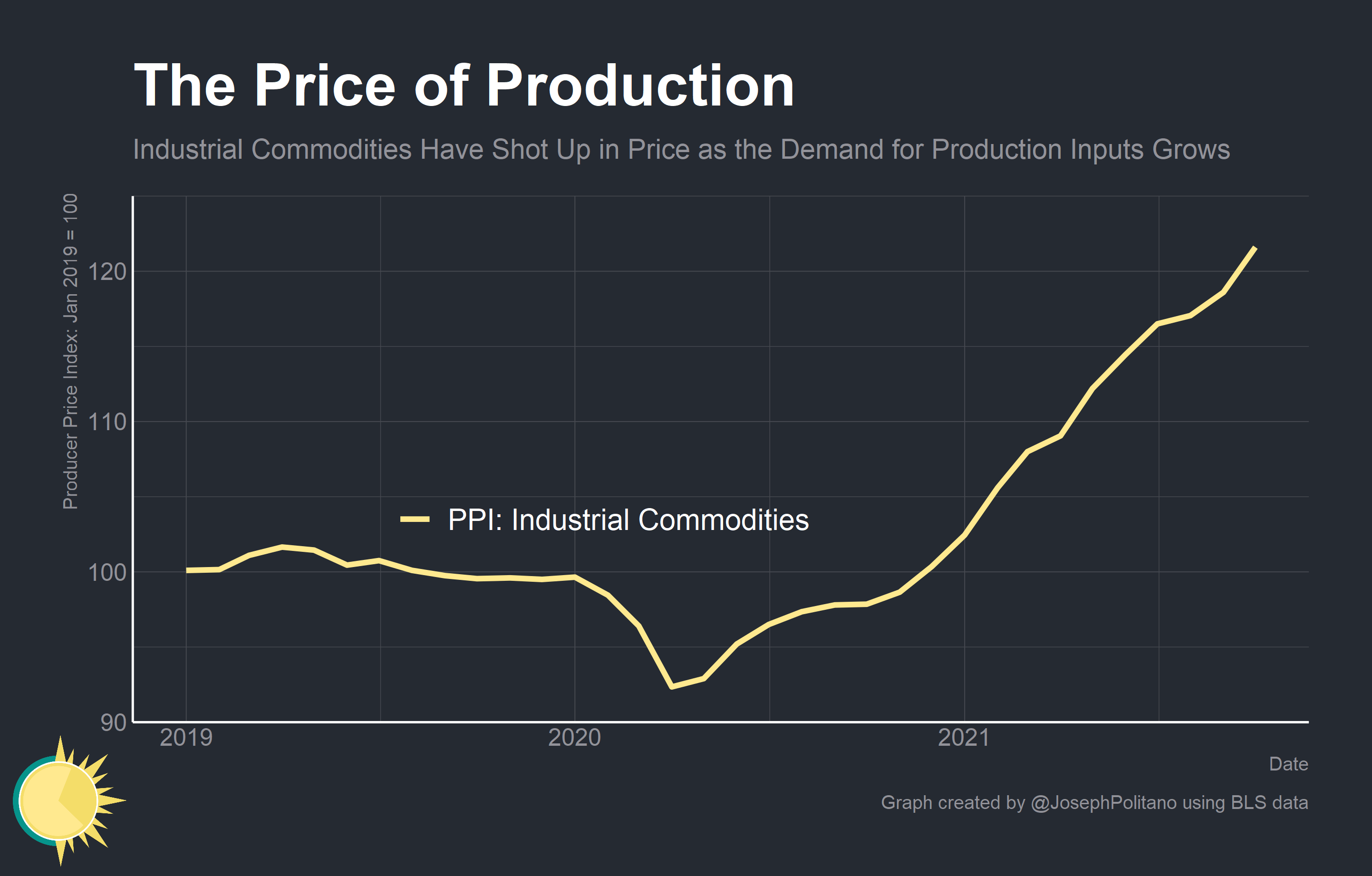

Producer prices for various industrial commodities have been on a tear for the last year as global manufacturers struggle to keep up with the rising demand and orders. This is an almost-unprecedented spike as commodity price indexes have remained fundamentally unchanged since the global financial crisis. Manufacturers are absorbing a lot of the price shocks to raw material inputs and not passing them fully onto final consumers, which is evidence that corporations do not currently expect either the elevated demand for final goods or elevated prices for raw material inputs to remain permanent.

{kind=link}

Automobiles and other used vehicles have been emblematic of the kind of accelerated demand and strained supply chains that have caused rising prices in the goods sector. After a massive drop in sales at the onset of the pandemic, demand for automobiles roared back in late 2020 and used car dealerships posted their best sales numbers in history. COVID-fearing travelers were worried about using airlines or other forms of public transportation. They flocked to purchase new or used cars, depleting dealerships’ inventory. Heightened demand for all sorts of electronics, gadgets, tools, and vehicles helped to drive a global semiconductor shortage that constrained automobile production—and the result was an unprecedented jump in prices.

Nowadays, car prices tell a different story. The number of cars sold has plummeted as a lack of inventory and rising prices have put consumers off. More people are regularly taking public transportation and, critically, parents are more comfortable letting their children onto school buses. Automobile prices have stalled out, with used car and truck prices growing 2.5% in October after declining in August and September. This is representative of industries throughout the goods sector.

Nominal spending on goods has stalled for several months while nominal spending on services and aggregate nominal spending have increased. This is partly because of the rising prices and partly because vaccinations are enabling additional services spending. While consumers have not spent down all their “excess savings” they also no longer have a higher-than-normal savings rate, so nominal goods spending is likely to revert to the pre-pandemic trend in the near future. Critically, many manufacturing firms and commodity producers may be experiencing a “bullwhip” effect whereby rising prices and shrinking inventories cause consumers to scramble to purchase additional items in an attempt to prevent going without (think of what happened to toilet paper or hand sanitizer during the beginning of the pandemic). In aggregate, this can cause massive transitory movements in prices as buyers scramble to secure their goods. After demand abates, prices crash as suppliers are left struggling to sell as prospective buyers had already stocked up on inventory as a precaution.

The Future Inflation Situation

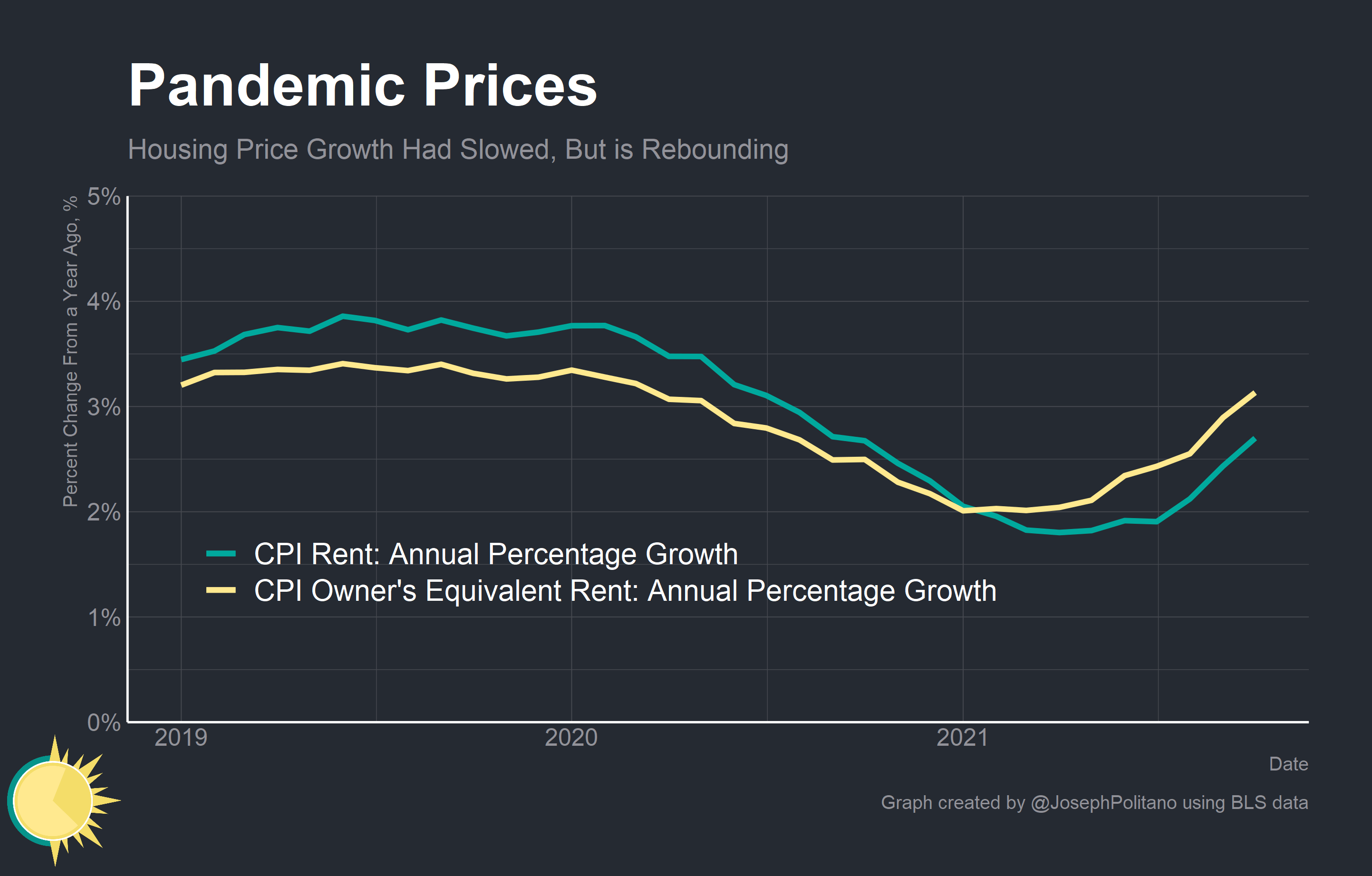

The rise in services spending has started to pull service sector prices back up to pre-pandemic growth rates as consumers’ spending patterns renormalize. Take housing: the lack of sufficient homebuilding has lead to increasing rents throughout the latter half of the 2010s. The pandemic initially reduced rent growth rates as workers exited high-rent cities and household formation was slowed by young adults moving back in with their families. As the economy strengthened and COVID abated, rents have climbed as workers return to cities and young adults begin moving out. Given that shelter makes up approximately 1/3 of the CPI’s basket, any movement in rent prices will have large effects on inflation measurements in the short term. That’s why it should be concerning that private trackers are showing large increases in rent prices (although they use different methodology than BLS that likely create a significant upward bias compared to CPI).

Most of Americans’ labor and spending is in services, and inflation has generally been concentrated in services over the last several decades. That’s why it is important to understand that rising incomes—and therefore wages—are the only thing that can support long run increases in rents and other service sector prices. We are currently seeing fairly strong wage and compensation growth at the individual level, but it is by no means outside historically normal levels—the last time growth in the employment cost index hit its current levels was in 2005. From an aggregate perspective, Gross Labor Income (GLI) is still below the pre-pandemic trend because of elevated unemployment levels.

To encounter the so-called “wage-price spiral” where rising wages beget rising prices in a vicious cycle, rising labor costs would have to be passed on to consumers by businesses across industries. However, the current evidence contradicts this: the abnormal price increases are concentrated in the goods sector while abnormal wage increases are concentrated in the service sector.

Fundamentally, sustained inflation cannot occur without above-trend income and spending growth. As of right now, both personal incomes and personal spending remain on-trend. The excess savings that manifested during the pandemic are mostly held by the top 10% of income earners, so they are unlikely to be spent down aggressively or interfere with normal labor market functionality, as some have suggested.

As long as policymakers in the Federal Reserve, Congress, and the White House ensure that nominal income growth remains on-trend inflation will slide back down to normal levels.

The wild card here is energy prices no? A lot of grumpiness from the general public is from gas prices - the stuff they see every day.

The inflation in goods of first necessity can crush consumer spending. Think the inflation caused by FX weakness or by elevated energy prices. It happened in many economies going through a crisis. Asset prices deflate, discretionary goods deflate. But the inflation is very palpable then. The salaries follow, under political pressure. Sometimes the sequence of events flips. :)