The views expressed in this blog are entirely my own and do not necessarily represent the views of the Bureau of Labor Statistics or the United States Government.

In January 1973, a volcanic eruption began without warning near the Vestmannaeyjar archipelago off the coast of Iceland. A large fissure started spewing molten lava only 1km away from Heimaey, an island of 5,300 people. The Icelandic State Civil Defense Organization sprung into action, carrying out a thorough evacuation of all residents within 24 hours of the initial eruption. Lava-cooling operations were undergone in an attempt to save the harbor at Himaey and residential sections of the island, but ultimately some 400 homes were destroyed by the eruption.

This year Emi Nakamura, Jón Steinsson, and Jósef Sigurdsson published an updated version of their working paper studying the people displaced by the 1973 eruption. They found, somewhat counterintuitively, that young people who were forced to leave Heimaey due to the volcano actually had higher lifetime earnings and more education than those who stayed behind. This is despite the eruption having a negative (though not statistically significant) effect on the earnings of older heads of households who left the island. How could losing your home in a natural disaster prove economically beneficial? Essentially, the decision to move benefitted young people who had a comparative advantage in jobs outside the fishing industry (which dominated Heimaey), and the eruption pushed them to overcome migration frictions that left them “stuck” and would have held them back in the long run.

In March 2021, the normally-unremarkable Economic Outlook report from the Organization of Economic Cooperation and Development (OECD) began turning heads online. The OECD’s projections for Gross Domestic Product (GDP) showed the United States exceeding pre-pandemic forecasts in the fourth quarter of 2021. In other words, they expected the US economy to be larger at the end of 2021 than they did before COVID-19 was first discovered. In May they revised their forecasts for American GDP even farther upwards, making the US the only country the OECD believed would leave 2021 with a bigger economy than they expected had there been no pandemic at all.

Eventually, these projections were brought back down to earth. With the outbreaks of the Delta and Omicron variant alongside supply chain crunches, economic growth suffered. The OECD now expects US real GDP to stay somewhat below pre-pandemic forecasts, but it is still remarkable that they could have ever expected the US economy to exit the pandemic stronger than it entered. How could a once-in-a-generation public health catastrophe end up being a net positive for the economy?

Of course, it is not—the pandemic itself has ended countless lives and wrought incredible devastation across the globe. It may take decades of study into the effects of long COVID, learning loss, and the pandemic’s economic shock before the true extent of the damage can be assessed. But the response to the pandemic—the policies, programs, and choices that were implemented by central banks, governments, businesses, and individuals—proved nearly enough to fully counteract COVID’s short-term economic damage. If we play our cards right, it is possible that the economy could be stronger than anyone could have expected.

The State Capacity Revolution

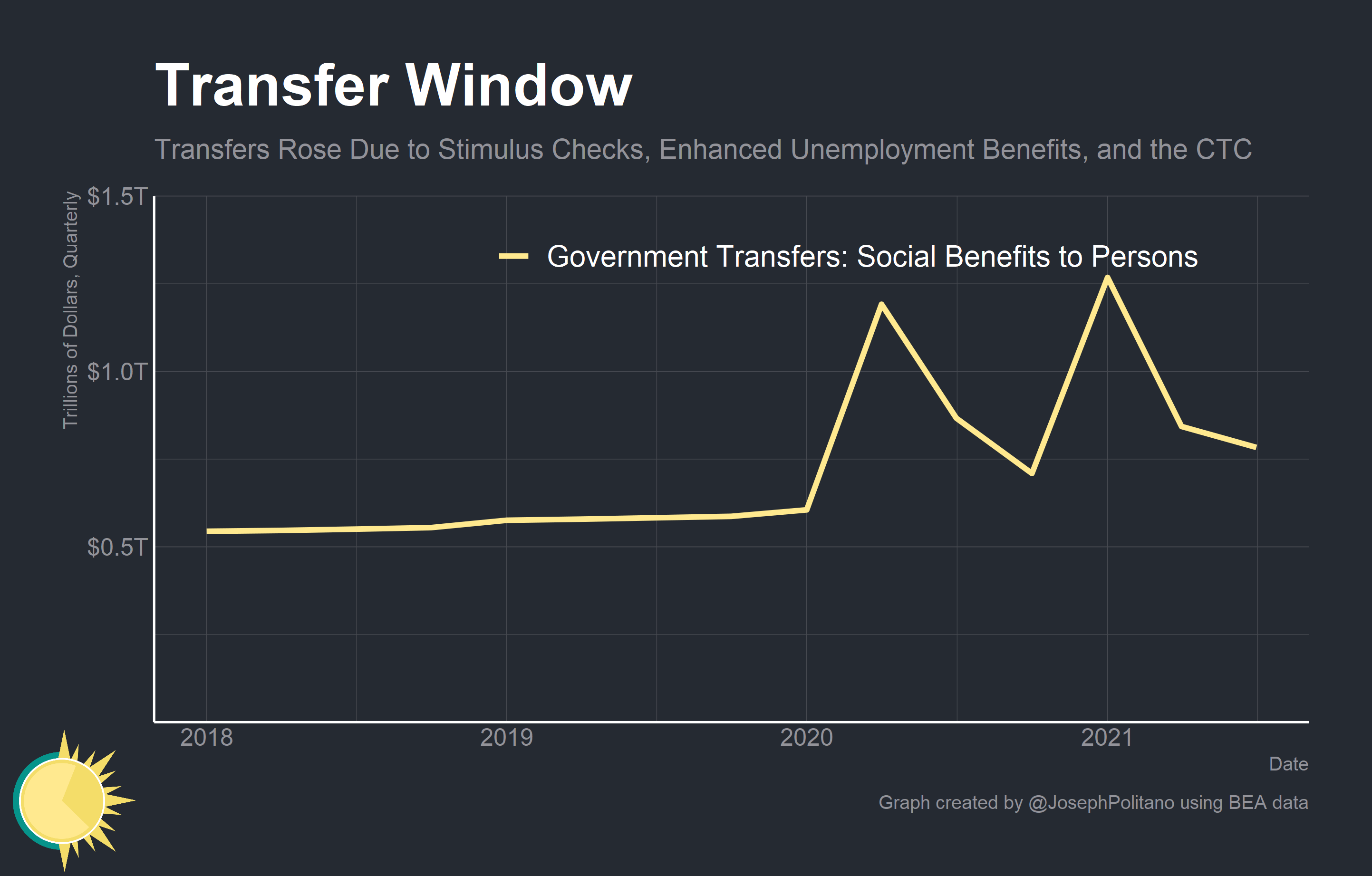

The federal government’s response to the crisis was nothing short of essential in preventing economic collapse and bringing about the robust growth we are experiencing today. Quarterly government transfers more than doubled as a result of the implementation of stimulus checks, enhanced unemployment benefits, and the child tax credit. These programs preserved household incomes and overall spending despite the pandemic, preventing the kind of self-reinforcing economic slowdown that characterized the 2008 recession.

The response to the 2008 crash was plainly insufficient when compared to the scale of the economic downturn. It took until nearly 2018 to achieve the job market recovery that has occurred in the time since COVID hit the US. Economist Paul Krugman joked in the aftermath of the Great Recession that an alien invasion would end the downturn—the fact that a financial crisis caused the economy to collapse meant that there was no easy, real threat for policymakers to coalesce against in order to cut through political jockeying and draft a response strong enough to meet the situation at hand. A similar issue occurred during the Great Depression, and it took the mobilization for World War II to get policymakers to put together a package strong enough to end the unemployment crisis.

COVID-19 was the alien invasion, and the US government responded strongly. The CARES Act, which sent out the first stimulus checks, established enhanced unemployment, and created the Paycheck Protection Program, passed with only 6 members of congress voting in opposition. A meagre 6 Senators voted against the Consolidated Appropriations Act that sent out $600 stimulus checks in late 2020, and it was only Biden’s American Rescue Plan that had to squeak by on partisan votes. Even bigger news came from across the pond where common EU debt—a policy long opposed by some of the most powerful nations in the bloc—was issued for the first time in order to fight the pandemic.

All of this is even more important in light of the “ratchet effect”—the tendency for government expenditures to expand during times of crisis and, like a ratchet, resist coming back down after the crisis has ended. In a world of aging populations and declining real interest rates, large government budget deficits may be necessary for macroeconomic stabilization. This shift has been resisted by political constituencies within many high income nations, but their resistance largely evaporated in the face of the pandemic.

Nor was the expansion of state capacity confined simply to the size of public expenditures. Throughout the pandemic, federal and state governments have worked to cut out bad policies and expand their reach unburdened by the usual political opposition of interest groups. State governments waived licensing rules that prevented out-of-state medical workers from serving in-state patients. The FDA moved at record speeds to approve COVID vaccines (although they still should have moved faster). City governments requisitioned hotels for homeless residents in order to protect them and stem the spread of COVID-19. Even the Federal Reserve, usually among the most conservative of institutions, made use of new tools in order to combat the pandemic.

The Financial Crisis that Never Happened

It is March 13th, 2020, and financial markets are in full-blown crisis mode. It’s not the normal kind of financial meltdown where stocks slide and the price of US government debt jumps as investors start valuing safety. No, even Treasury bonds are sinking in price as market participants start desperately looking for cash. Federal Reserve officials in New York, Washington, and across the country are watching the crisis unfold and scrambling to implement measures in order to prevent a complete financial meltdown. The order was functionally to save everything.

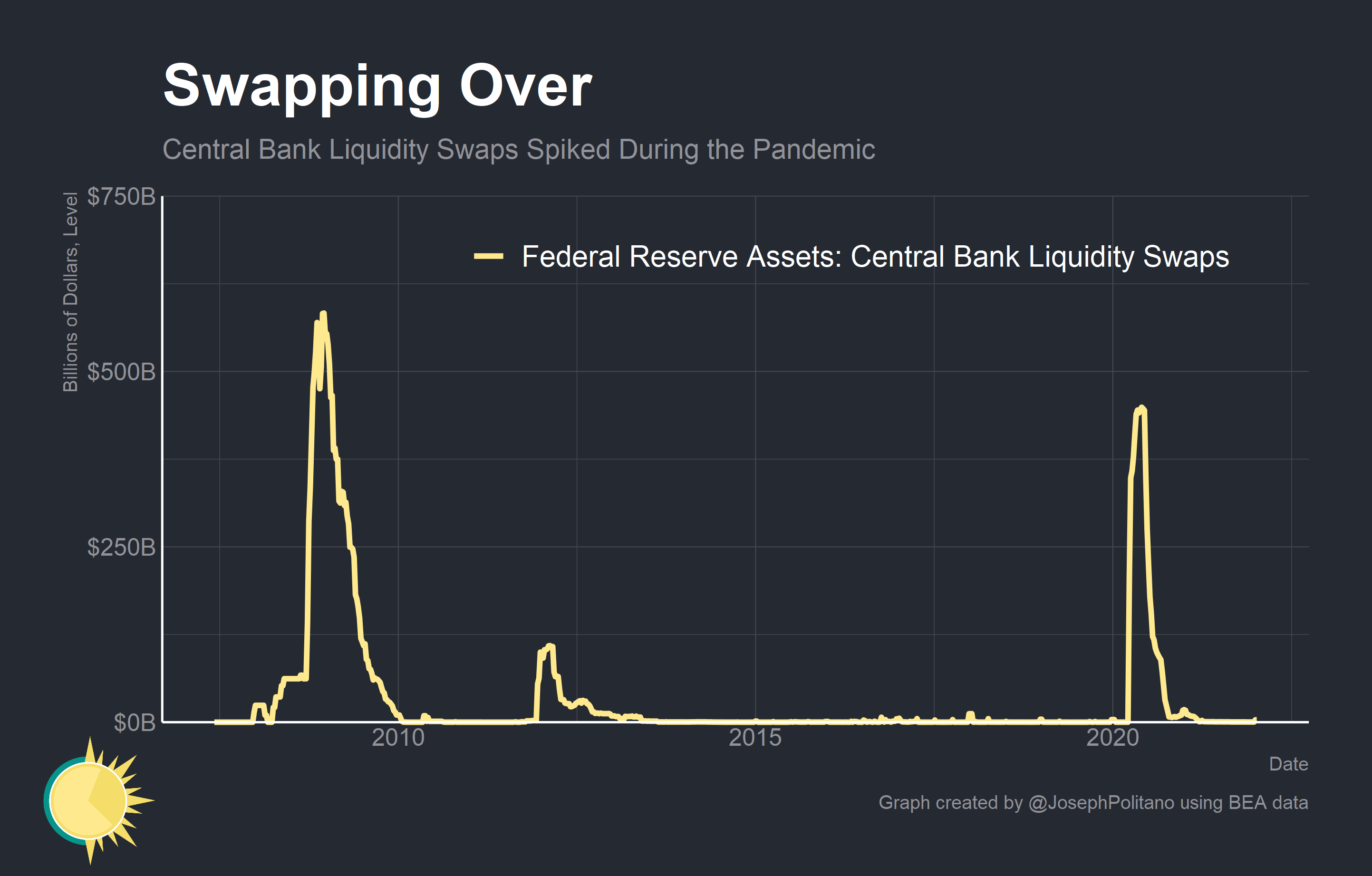

Interest rates were slashed to zero. The Fed began engaging in massive levels of liquidity swaps, essentially lending cash to a wide array of foreign central banks in order to backstop global dollar funding markets. The Federal Reserve Bank of New York was authorized to buy as many Treasuries as necessary in order to stabilize government debt markets and expanded repo operations (short-term loans collateralized by Treasuries) to ensure that market participants had constant access to credit. They opened a veritable alphabet soup of emergency facilities—the Municipal Liquidity Facility to support lending to state and local governments, the Main Street Lending Program to support lending to small businesses, the Commercial Paper Funding Facility, the Money Market Mutual Fund Liquidity Facility, and several others. The Federal Reserve even opened facilities to intervene in corporate bond markets.

The result? Despite extreme market turbulence, the Federal Reserve managed to avoid a complete meltdown in credit markets. No banks, major financial institutions, or funding markets collapsed (though heavy intervention was required to rescue Money Market Funds). Financial woes were less of a concern than the employment and inflation situations, and the US dollar is entering 2022 more dominant than it entered 2020. The Federal Reserve proved that it was willing to backstop any dollar-denominated market within its jurisdiction, and participants are not likely to forget this the next time financial markets go haywire.

It was this financial backstop that enabled the Federal Reserve to pursue the stimulative monetary policy that has been critical to the rapid recovery in employment and real output. Without functioning financial markets Jerome Powell’s pursuit of a full-employment recovery would not have been possible, and it was the great expansion of the Federal Reserve’s capacity early in the pandemic that enabled it to support the real economy.

Life After the Volcano

Government entities are not the only organizations that were spurred into action by the pandemic—individuals and businesses have been pushed to change for the better in response to COVID-19. The pandemic accelerated preexisting trends such as the transition to remote work and shift to e-commerce, forcing consumers and businesses to adapt to the modern world faster. More than that, the pandemic kickstarted several brand-new positive economic trends.

Business formation, extremely sluggish in the superstar firm-dominated economy of the 2010s, shot up shortly after the onset of COVID-19. Unemployed workers were forced to find their own opportunities, and stimulus checks or enhanced unemployment benefits provided the perfect starting capital for many entrepreneurs. Nor were these simply creations of desperation—business applications have remained high despite significant improvement in the labor market, and high propensity business applications (those from firms that are likely to hire employees) are also elevated. Plenty of new companies are likely exploiting digital distribution channels to reach larger audiences, increasing competition and variety within the American economy.

Even those who remained at 9-5s did not necessarily keep the same jobs. The quits rate has been steadily increasing since the start of the pandemic as a strong labor market enables workers find more productive and higher paying jobs. Workers are also moving to lower-cost, faster-growing cities with more opportunities for individual and aggregate economic growth, upending the prior trend of labor market opportunities being concentrated in a few expensive superstar cities. Just like on the island of Heimaey, an unexpected push may be just what some people needed to seize a new opportunity.

Firms, for their part, are investing in modernizing their infrastructure, organizational structures, and practices. The transition to remote work has facilitated changes in hiring, retention, engagement, and communication throughout companies. Though it will take time (and the end of the pandemic) for the dust to settle, it is possible that remote work trends will enable a work environment that is both more productive and equitable.

Of course, the increasing utilization of the internet and technological resources has spurred renewed investment in research and development. Unlike in the aftermath of the 2008 recession, the COVID era has seen an acceleration of GDP in the research and development sector. The strong demand environment is forcing firms to innovate in order to compete.

Conclusions

None of this should be construed to say that the pandemic—or Icelandic volcanic eruptions, for that matter—was a “net good.” The pandemic is nothing short of a global disaster on an unprecedented scale. It is the policy response to the pandemic from institutions—a response that could theoretically have come regardless of COVID—that is pushing the world forward. In other words, World War II did not end the Depression. It merely provided justification to implement policies that ended the Depression—policies that could have been undertaken war or no war.

Nor should the changes that have come about as a result of the pandemic be taken for granted as COVID recedes. Public programs—like the wildly successful Child Tax Credit—are at serious risk of expiration in today’s hyperpolarized political environment. Efficiency within government programs could begin backsliding once the public eye looks away, and business investment could be cut back if the economic situation deteriorates. The Federal Reserve already had some of its discretionary powers stripped away.

The role of economic institutions in a democratic society is to encourage the kind of growth that we are seeing today—without requiring an extreme crisis in order to be spurred into action. The lesson of the pandemic should be that the political economy oftentimes matters more than the actual economy—and that creating institutions to better channel the political economy is critical to sustainable long-term growth.

you keep finding ideas i don't see anywhere else, great work!